8 of my favorite tools for financial wellbeing (#6 Could change your life…)

Alright, alright—let’s jump into this.

One thing you may not know about me is that I take my finances verrrrrrry seriously. While a lot of my life I live in a very go-with-the-flow & relaxed manner, I think it’s so crucial to have *structure* and a general plan around your finances. And trust me, I was NOT always like this. While I have always admittedly done pretty well at living within my means (having odd jobs, paying my own way through college, finding good deals, etc.), I didn’t really ever have a concrete PLAN for my money until about 2017.

However, with time, I’ve learned to invest (pun intended) in my finances and to pay attention, spend intentionally, save (both short-term and long-term) and be PROACTIVE with my finances. Because beyond “the basics” that money can buy, money can impact things like your health and overall quality of life—it truly touches every aspect of wellbeing. And while you may think it’s odd that I regularly talk about money on a health & wellness blog, I really really really consider taking responsibility for your finances as one of the ultimate forms of self-care. You can’t fulllllly take care of yourself if you don’t fully have a grip on yo’ dollas.

While there are a lot of factors to consider when it comes to finances, and it is important to consider privilege, wage gaps, systemic injustices, unequal access to resources, and countless unique situations, costs, incomes, etc., there are a few tried and true tools and hacks that I think will be useful to pretty much everyone! I’ve used the resources below over the years to increase my net worth, my financial knowledge, and truly equip myself to handle my money with abundance and joy.

The first two ideas on this list are basic, foundational money habits just to get ya rollin’—then the remaining items on the list are more unique, specific ideas! (#6 is hands down my best-kept money secret…)

So, without further ado, here are 8 (millennial-approved) money hacks to help you rock your finances.

#1 crunch the numbers!

This may sound simple, but it’s one of the most effective ways to get a sense of where you are financially. Grab a pen, a notebook, and your fave beverage and create a list of ways money comes in each month (your salary, side hustle, spouse’s income, etc.) AND ways money goes out each month (rent, bills, groceries, eating out, etc.) and then add up the average monthly amounts to get a sense of whether you’re making more than you’re spending—or vice versa.

This is how any good adventure starts—with research. This step is allllll about sitting down and calculating monthly expenses. Let me just start this out by saying that I think this is a GREAT exercise for anyone. While it may seem intimidating to sit down and get a good look at your finances, you’ll likely end up feeling so much freedom when you really break down where your money is going + know how to move forward.

Now this isn’t a budget per se, but this is where you can estimate allllllllll of your monthly expenses—no matter how big or small, it’s important to see where you are at in terms of money in and money out. Take a look at your average money spent in different categories over the last 1-3 months. If you want an in-depth example category list, peek at my old post here. :)

Then, what you’ll do:

TOTAL MONTHLY INCOME (after taxes are taken out) - TOTAL MONTHLY EXPENSES = LEFTOVER MONEY

This is a powerful exercise because you might have an idea of what you’re spending each month, but when you truly look at money in versus money out with cold, hard math, you’ll see a clear picture of your financial health. You will see immediately if what you earn is adequate enough to cover these costs or not. If you end up with a negative number, you know that you've got to make some adjustments. Basically: if that leftover money isn’t as high as you’d like it to be—where can you adjust?

#2 take some pen & paper time to reflect & look big picture

While above we tried to be specific and consider ALLLLLL the little monthly costs you may not be thinking of, next we will zoom out a bit. Once you feel good about the list above, categorize your expenses into 3-6 general domains for budgeting purposes: for example, living costs (rent/utilities), bills (including subscriptions + fees!), food (groceries, alcohol, eating out, etc.), miscellaneous “extra” money (like going out to eat, travel, clothing purchases, Amazon, etc.), and then a savings & investments category (yes, I believe you should BUDGET and plan for this area!). I see people often get WAYYY too specific with budgeting categories and then get burnt out trying to categorize all the small, niche categories. I think it can be more helpful to be BROAD in your money categories and have 3-6 general expense areas and create general monthly budgets for these areas.

This may take a while at first, but getting these expenses categorized provides SUCH a helpful look at whether you’re truly staying within your means, to see where you’re overspending, to quantify how much you can be saving/investing (WITHOUT having to budget yourself to death). Create some general budgets for the categories above—maybe compare where you are currently at to where you want to be. Then, commit for the next month to stay within these boundaries you set! You’ve got this!

Optional, but once you write this list of expenses/income and create your general categories, it may be powerful to do some journaling or reflecting on the following prompts:

Be honest— how do I feel about my financial situation right now?

Are there any obvious places where I am overspending? What are 3 tangible ways I could work to limit this?

Where do I see room for growth in my money journey? (This could be tangible, super specific, more mindset-focused, etc. Anything goes! This is your money story!)

What is something that I am doing well with my finances? (Go ahead! Pat yourself on the back!)

How do I want to feel when it comes to money? What are tangible action steps I can take to work towards that?

What are 1-2 money goals I want to set? (Make these goals in SMART format—Specific, Measureable, Attainable, Realistic, and Timely. Example: “In the next 6 months, I will save $5,000.”)

#3 create a Personal Capital account

WOWOOWOW. I loveeee this website. FYI, this is not sponsored—just a gal recommending a helpful tool to another friend! Personal Capital has been an absolute game-changer in my finances. I mentioned Personal Capital in a recent email to my email club (pssssst...sign up here to get on the list if you have a lil’ inbox FOMO!) because it’s SO great at providing a big-picture look at your finances.

HOW IT WORKS: This app links to alllllll of your different financial accounts (savings, retirement, your spouse’s retirement, your credit cards, your mortgage, all of your banks…) and comprehensively tracks your TOTAL net worth so you can check in without having to log in and out of all of your different accounts and manually add them up.

It also compiles ALL of your transactions so it’s a super simple place to budget as your debit cards, credit cards, bank accounts are all in one place. I’ll admit, I was a bit inconsistent with budgeting, but by having everything linked to one place, it’s been a game changer. This is where I categorize & keep track of the 3-6 general budget domains I set in step #2 ^^^. If you are having trouble compiling your expenses, seeing where your money is going, or struggling to create spending categories/budgets in the steps above, this website is CLUTCH as everything is one place and automatically accounted for.

I could ramble forever— but this website is SUCH a time-saver, 100% free, and so helpful to see information on every account all in one place. I take a peek at Personal Capital on the first of every month to track my spending and make sure my net worth is going up month-after-month. It’s SO easy, and the best part? It’s totally free. (Click this totally unsponsored refer-a-friend link to get a $25 Amazon gift card when you sign up!). Hiiiighly recommend this platform. :) It’s hard to measure your progress if you’re not even tracking it—and this is a super user-friendly way to do that!

#4 inspirational (and easy to understand) financial Instagram accounts

One of the biggest steps to financial wellbeing is financial literacy. And before you jump to “but, Kate, I am SO clueless and bad with money!”, I want you to stop right there. Because you ARE smart. You ARE capable. And you CAN learn this stuff. I want you to release the guilt of what you think you “should” know, and instead just give yourself permission to be where you’re at—then look forward.

I used to be soooooooo intimidated by finance concepts. The vocab, different types of accounts, learning how to invest???? I had ZERO clue what any of it meant, but I committed to approaching it with a growth mindset. I truly started at ground zero, but by exposing myself to different money books, finance accounts on Instagram, and podcasts on the regular, I now know the difference between a 401K and a Roth IRA (*takes bow*). While I still have a long way to go, I can truly say regular exposure to these financial lessons has been SO empowering and impactful to my overall money mindset.

One way to simplify financial concepts is to surround yourself with financial information, terminology, and mini-lessons via social media and the content you consume. While there is a looooot of financial gurus out there, here are a few resources I recommend following to get some great finance info on the daily:

Money with Katie: Hilarious, tangible, and millennial-approved—I LOVE reading her posts.

Personal Finance Club: Super concrete + simple—he really walks the walk and makes amazing graphics for all of my fellow visual learners!

Female In Finance: This one goes out to my ladiesssss. As a whole, women are underpaid, under-confident, and under-taught about finances (don’t even get me started on the gender pay gap…). I’ll save you a 3 paragraph soapbox rant, but I love that this account is about finances for women, by women. Super concrete, realistic, and fun way to learn about money.

Ramit Sethi: Basically, my money icon. Ramit is SO good at explaining higher-level concepts + money psychology and making it SUPER simple...plus he’s the author of my FAVE financial book which maaayyyy be outlined in the next paragraph…

Cartoon credit: Christopher Weyant

#5 THIS. BOOK.

I’ve mentioned I Will Teach You To Be Rich by Ramit Sethi at LEAST 10 times before, but it’s just. that. good. This book is fun, easy to read, digestible, and really teaches you how to build a rich life for YOU—not as in making millions of dollars, but as in making the most of YOUR finances in a way that supports the life you want to live and sets you up for future success. I couldn’t love or recommend this book more—so tangible, so easy to understand, and SUCH a goodie.

book / kindle / audio

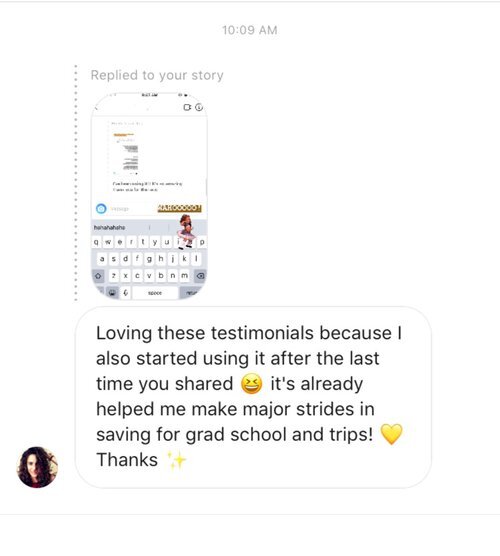

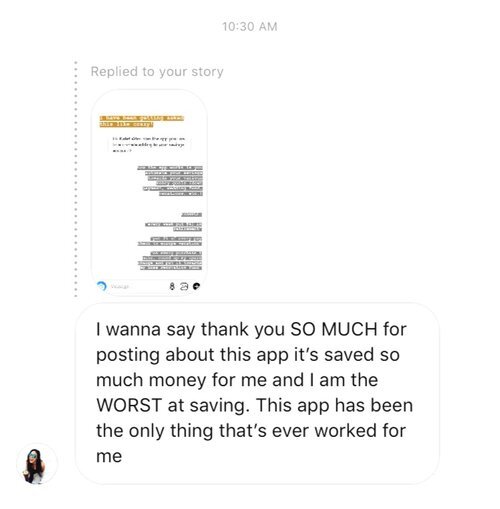

#6 if nothingggg else, i recommend getting this specific app…

Get. the. app. Qapital. Seriously, stop what you’re doing (aka stop reading this blog post, and go download it now). Again, I’ve talked about this app a millllllllllllion times...but for good reason (and again, this isn’t sponsored, but I wish it was...Qapital, if you’re reading this, hit a girl UP!)

HOW IT WORKS: Once you download the app, you customize what you’re saving for (wedding, down payment, Hawaii, etc.), set the amount of money you want to save for that goal, and customize how you would like to save towards it, thennnn (DRUM ROLL), the app will automatically start saving from your bank account, and you just sit back and watch your money pile growwww.

I truly LOVE this app for so many reasons, but most of all is how it’s SIMPLE and really meets you where you’re at. (Like, “saving-$10-per-week-because-I’m-a-broke-college-student” where you’re at). So whether your weekly savings are $10 or $1000, Qapital allows you to save for YOUR savings goals wherever you are at this point in your life.

It makes saving money EASY— yes, even for those people that just “suck at saving money.” In fact, the AVERAGE Qapital user saved $4,300 in their first year alone (yes, really). You’re gonna love it. :) For a limited time, get $25 in your account for free when you sign up with this refer-a-friend link. :)

but don’t just take it from me… ;)

#7 the Acorns app for beginner investing

If you’ve been thinking about getting into the investment game but you don’t know where to start, Acorns is the app for you. It takes allllllll of the intimidation out of investing and helps you invest your money with ease. I’ve loved using this app because of how customizable it is—I can round up my purchases, invest $20 a week, or whatever feels right for me.

Acorns automates everything and just makes investing so simple. Do I think it is THEE best place for all of your long-term investing goals (401K, Roth-IRA, etc)? Nope, probably not! But this app is a perfect place to START investing because it makes it so simple & easy for those that are intimidated by more advanced investment platforms. If you know you should be investing, but have felt too intimidated to start— this app is such a great way to get dip your toes in!

#8 start tracking your progress!

“If you don’t measure it, you can’t improve it.” Mmmmm, this step is CRUCIAL. And while it may feel intimidating at first, it will soon become the most EMPOWERING step as you see your progress, net worth, and financial situation grow and improve month after month! For this, I recommend setting a monthly reminder on your phone for the 1st of the month where you review the spending for the previous month, check in on your net worth in Personal Capital, your savings goals in Qapital, and record your total expenses, income, and net worth each month in a notebook, note, Excel spreadsheet, or whatever works for you!

It doesn’t matter where you write it down, but the important thing its to RECORD it and be consistent. You’ll be able to see realistic trends— how you’re spending, investing, saving, etc. Once you get used to it, you will low-key get EXCITED to do this step as you will be seeing your financial progress in front of your eyes. You’ve got this!

to wrap it up!

Well, there ya have it, friend! Eight tools I’ve used to improve my financial literacy and feel more abundant with my money. Whether you use one, two, or all eight, I hope these hacks will help you feel more confident + joyful with your monay, honay!

ready for more?